Digging for Defense

DoD-subsidized mining under Defense Production Act

Something in the news caught my eye last week and I realized that something has largely been flying under the radar, for most of us.

Last week, I saw a couple of news releases indicating that the Department of Defense had issued grants to mining companies totaling more than $110 million to increase the production of critical minerals, specifically Lithium and Nickel.

Let’s take a quick look at how and why the DoD is getting involved in mining.

Over the past few years, the DoD has made several investments into private companies working to identify deposits, extract critical minerals, and ensure the supply chain resilience.

These investments are generally made under the Defense Production Act.

The Defense Production Act (DPA) came into law in 1950, during the Korean War and provides the Executive Branch (i.e., the Presidency) with some pretty broad authorities related to mobilization of industry to ensure the nation’s defense.

For example, the executive branch could force businesses to accept and prioritize contracts deemed necessary for national security, even at a loss to the business. Former President, Donald Trump, did just this in April of 2020, when he invoked the DPA to force 3M, General Electric, and Medtronic to produce more ventilators and N95 masks amid the early phases of the COVID-19 pandemic.

And, the DPA can be used to make investments into needed capabilities. During the Cold War, the looked like investments into mass mobilization capabilities. Following the Cold War, there was a shift towards investments into critical materials for advanced weaponry, such as rare earth elements, gallium arsenide semiconductors, superconducting wire, and more.

In February 2021, President Biden issued Executive Order 14017 on America’s Supply Chains, seeking to increase production, build in redundancies, secure networks, and strengthen resilience. In the Executive Order, the president specifically discussed rare earth elements (REEs), critical minerals, and other strategic materials. A month later, the President extended DPA coverage to those strategic and critical materials including lithium, nickel, cobalt, graphite, and manganese.

As a result, we can see a clear increase in the size and pace of the DoD’s investments into companies mining these minerals.

Sep 2023 - Albemarle Corp - $90M - Lithium: Kings Mountain, NC

Sep 2023 - Talon Nickel - $20.6M - Nickel: Tamarack Intrusive Complex, Minnesota

Jul 2023 - Graphite One - $37.5M - Graphite: Alaska

Jun 2023 - Jervois Global Ltd - $15M - Cobalt: Idaho

Dec 2022 - Perpetua Resources Idaho, Inc - $24.8M - Antimony: Idaho

- - - - - - - - - - - - - - - Presidential Determination (March 2021) - - - - - - - - - - - - - -

Feb 2021 - Lynas Rare Earths - $30.4M - Light Rare Earth Elements: Texas

Nov 2020 - MP Materials - $9.6M - Light Rare Earth Elements: California

Nov 2020 - TDA Magnetics - $2.3M - REEs: California

Since EO 14017 and the Presidential determination, the DoD has invested $187.9M into mining companies.

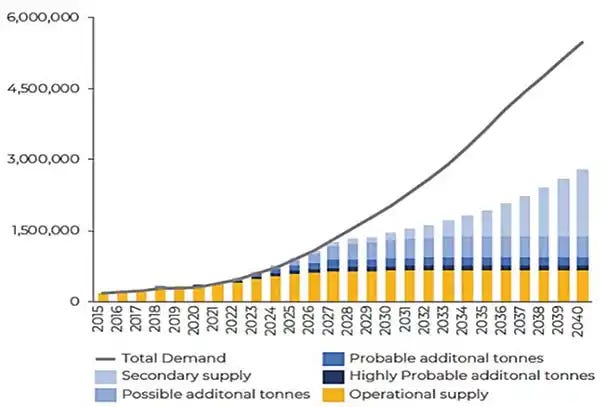

Most casual observers are likely familiar with the role that lithium plays, and why we’re classifying it as a critical mineral and investing in it.

Electric Vehicles are all the rage, right now. And these electric vehicles (or EVs) are reliant on lithium. In fact, the EV industry currently accounts for about 65% of the demand on lithium. As more and more markets implement mandates curbing gasoline / diesel powered vehicles, we can predict increasing demand for that lithium.

Producers are already struggling to keep pace with demand, and projections suggest that by 2030, there will be at least a 500,000 metric ton annual shortage.

Fortunately, we discovered last month that the McDermott Caldera, which straddles the California-Oregon border, has 40M metric tons of lithium. This deposit is now the largest deposit of lithium in the world and contains more lithium than all of the known deposits in China. But this remains a strategic mineral, and we must be judicious in our extraction, processing, and production using it. It remains to be seen, how quickly the United States can jump start its capacity for processing the material. Currently, we are highly dependent on China for its processing.

The material remains critical for our defense as we look at transitioning many of our military fighting vehicles to electric-drive systems, proliferate robotics reliant on batteries, and establish microgrids. Additionally, we use lithium in armor plating, ballistic glass, lubricants, and elsewhere.

Similar to lithium, nickel is used extensively in batteries and in armor. It’s resistance to corrosion leads to its use in jet engines and power facilities, where it is exposed to harsh elements for a long time. The United States currently imports around half of the nickel that we use (fortunately from diverse allies), and there are currently very little deposits in the United States that we can exploit.

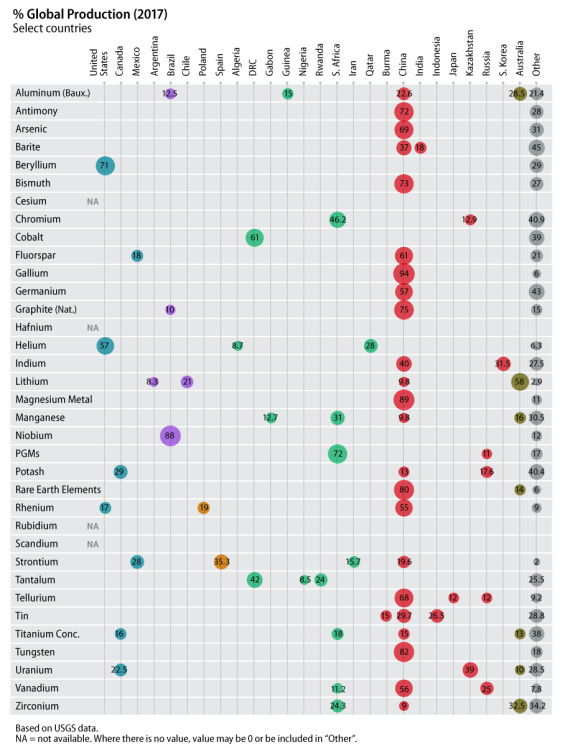

Graphite, antimony, cobalt, along with other important minerals (dysprosium, iridium, neodymium, magnesium, platinum, gallium, and on and on) all represent significant risks to our supply chains. We need these materials in their raw forms and, more importantly, in their refined forms. We are overly reliant on adversaries to produce these minerals, critical to our defense and energy resilience.

We are overly reliant on our adversaries. As such, the Department of Defense’s subsidization of certain companies in the mining industry is a great way for us to ensure that we’re able to keep building our defense.

The Manufacturing Capability Expansion and Investment Prioritization office, which falls under the Assistant Secretary of Defense for Industrial Base Policy, leads these Defense Production Act investments into six areas including Critical Minerals and Materials, but also Kinetic Capabilities, Microelectronics, Castings and Forgings, Energy Storage and Batteries, and Workforce. If interested, you can find more information here.

Keep building!

Andrew